Higher capital investment masks slowdown in spending

CoStar Analytics

A handful of data releases last week painted a broad-brush picture of a relatively resilient U.S. economy managing to muddle through a temporary energy price shock.

But a closer look at the details reveals a more nuanced picture, showing the balance of economic activity shifting toward capital investment as consumer spending weakens.

Consumers remain largely employed and continue to open their wallets, but revisions to earlier data showed spending was slower than initially reported. Moreover, this followed downward revisions to April data, together suggesting a significant slowdown in consumer spending as higher prices dent pocketbooks.

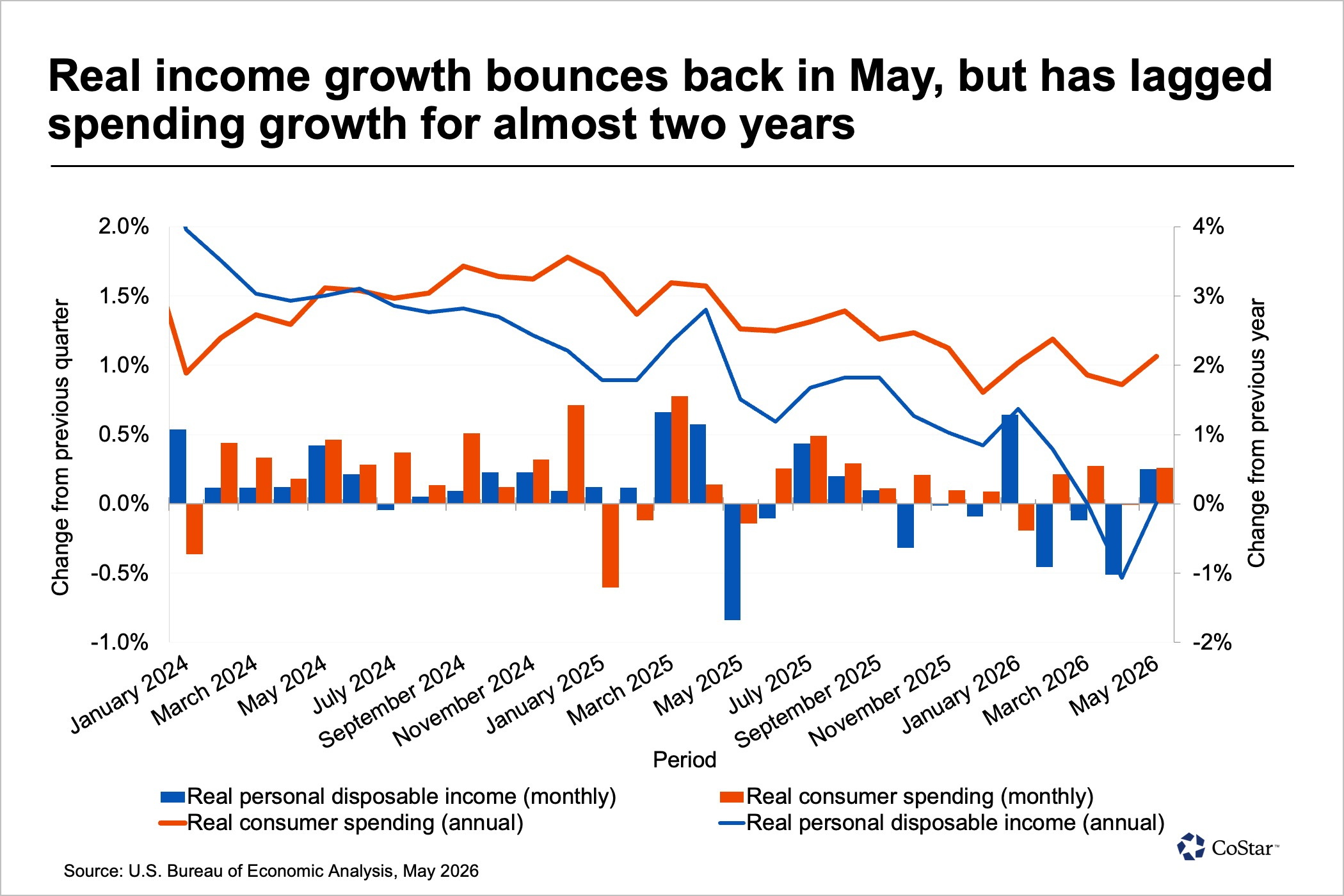

The Bureau of Economic Analysis’ initial report on consumer balance sheets for May revealed the first monthly increase in inflation-adjusted disposable personal income since before the start of the military conflict in Iran. Yet it was flat compared to a year ago.

Nominally, the increase was 0.7%, outpacing inflation for the first month since January. A one-time farm subsidy payment artificially boosted that total, more than doubling farm proprietors’ income and accounting for one-third of monthly personal income growth.

By comparison, wages and salaries, which typically account for the bulk of personal income, were flat on an inflation-adjusted basis.

Overall expenditure growth matched income growth at 0.7%, or 0.3% adjusted for inflation. While increased tax refunds may be helping to support spending this spring, consumers are using a combination of dipping into savings, shifting spending away from higher-cost discretionary items and taking on more debt to maintain spending levels.

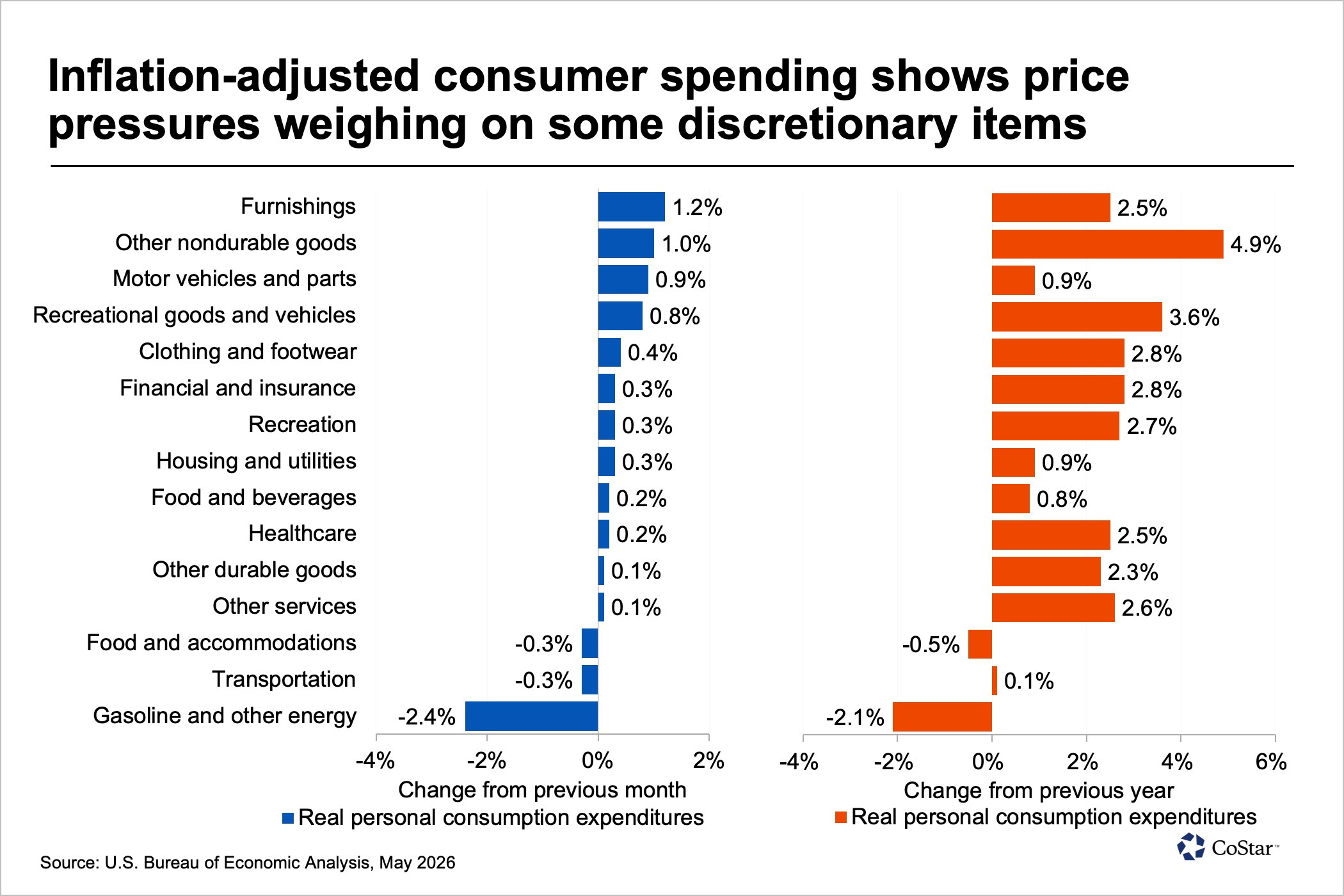

Despite rising income growth, the personal savings rate remained flat at a four-year low of 3%, down from 4.9% in May 2025. And though nominal spending on gasoline and other energy costs rose nearly 40% year over year, inflation-adjusted spending on gasoline and other energy declined by 2.1% year over year, indicating that some consumers had deferred trips or reduced energy use to cope with higher prices.

The 0.5% decline in real spending in hotels and restaurants suggests consumers are shifting spending away from some discretionary services as budgets are squeezed.

Softer consumer spending predated the intense energy price spikes of the past several months. While revisions to estimates for gross domestic product in the first quarter lifted the annualized growth rate from 1.6% to 2.1%, that upward revision was almost entirely due to lower imports and higher capital investment, as artificial intelligence-related spending on structures and equipment remains strong.

Consumer spending growth for the quarter was revised downward to an inflation-adjusted 0.5%, a four-year low.

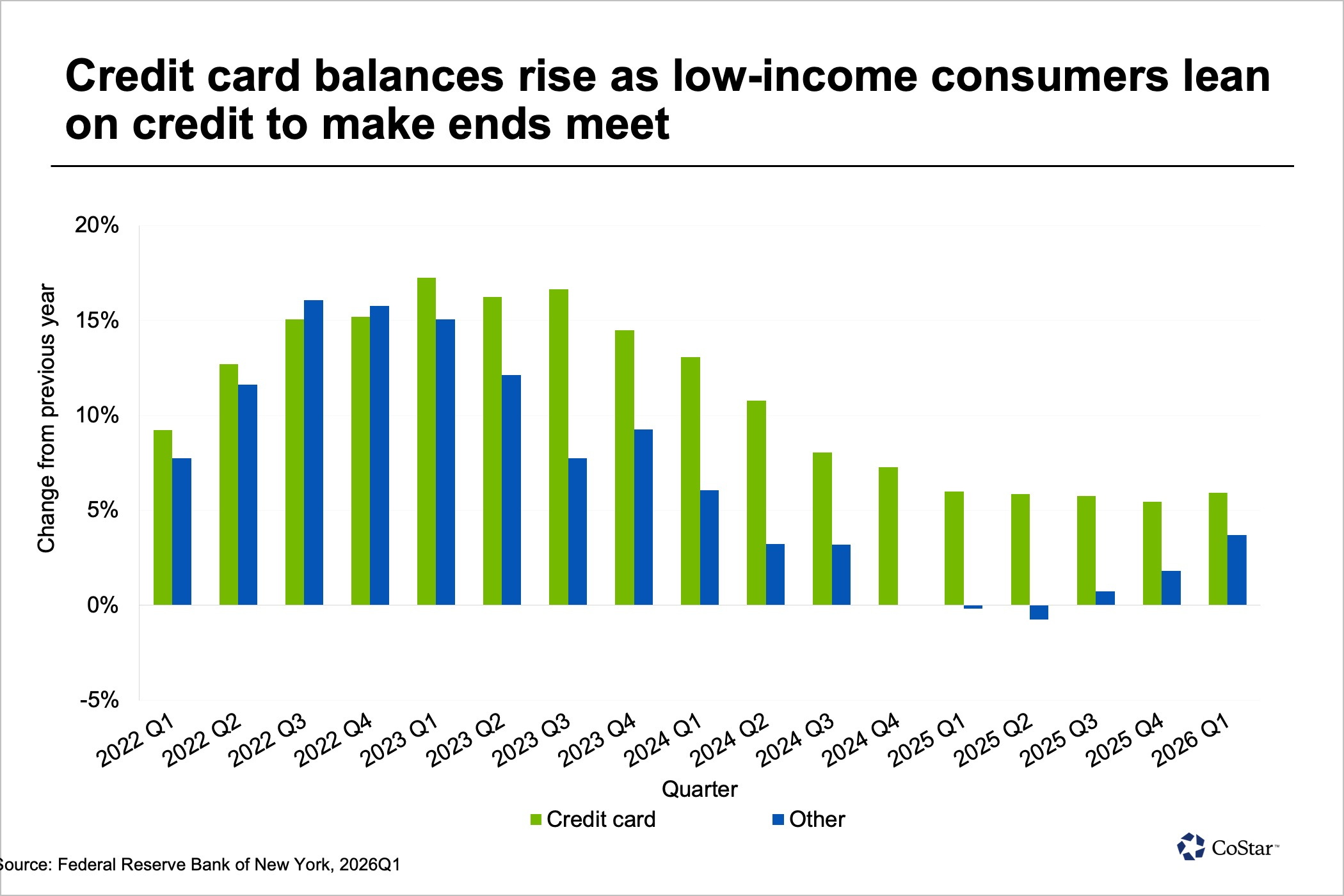

Though overall consumer debt has remained relatively stable over the past year, balances on consumer debt disproportionately held by lower-credit borrowers have moved higher.

Overall credit card balance growth has been stable over the past year, growing 5.9% annually through the first quarter, according to the Federal Reserve Bank of New York’s quarterly report on household debt and credit. Balances in the “other debt” category, which includes the unsecured personal loans lower-credit borrowers are more likely to take out, increased by 3.7% annually, the highest year-over-year increase since the first quarter of 2024.

While the recent stabilization of the labor market since March may also have helped to maintain spending levels, the consumer market remains highly bifurcated, with higher-income households enjoying the wealth effects of higher equity and asset prices and accounting for a large share of the consumer market, with the top 10% of households by income estimated to account for roughly 40% of all spending.

Lower-income households with fewer assets have been increasingly turning to credit cards and loans to fund daily needs. With interest rates on credit card balances north of 20%, these consumers are at risk of falling behind in payments. The share of credit card balances falling into severe delinquency, or 90 days or more delinquent, has reached 13.1%, a rate not seen since the Great Recession.

What we’re watching …

As the ceasefire in the Middle East is largely holding and at least some crude oil is making its way through the Strait of Hormuz, crude oil prices have fallen to trade near $70 a barrel, near pre-war levels. Still, the impact of higher energy costs is likely to take some time to fade from consumer prices.

The 4.1% rise in prices reported in May is likely to represent a peak. Other inflation pressures, including higher fertilizer costs still making their way into food prices and a global shortage of chips boosting prices of AI-related products, remain in play.

The combination of weaker consumer spending and still-elevated inflation will keep the Federal Reserve eager for more clarity in the coming months. Markets are fully expecting its next move to be a rate hike by year’s end.

CoStar Economy is produced this week by Christine Cooper, CoStar’s managing director and chief U.S. economist, and Chuck McShane, senior director of market analytics.